In my current career as an airline pilot, it’s the same with aircraft; if you don’t like aircraft, you shouldn’t be a pilot. And yes, I do fly with maximizing your section 179 deduction in 2021 people who don’t care much for aircraft! Common shares may also be referred to as common stock, ordinary shares, junior equity, or voting shares.

Journal Entry for Issuance of Common Stock

In Chapter 12 “In a Set of Financial Statements, What Information Is Conveyed about Equity Investments? ”, “accumulated other comprehensive income” was discussed because it was utilized to record changes in the fair value of available-for-sale securities. Gains and losses in the worth of these investments were not included within net income.

Journal entry for the issuance of common shares without par value

The common stock that company buyback from the market is recorded as treasury stock in the balance sheet. It is the negative balance report in the equity section in the balance sheet. The company needs to record the assets value, common stock, and additional paid-in capital, which is the same as the stock issue for cash. However, the transaction amount depends on assets market value or common stock market value whichever can be measured more reliability. Issue common stock is the process of selling the stock to the capital market. Only listed company can issue stock to the capital market and the investor will be able to purchase the share.

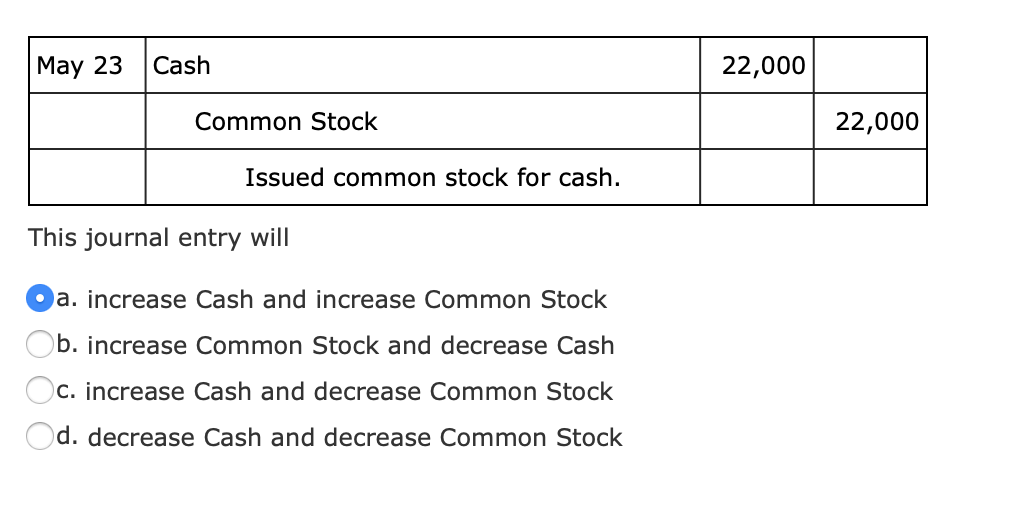

Issuance of common stock journal entry

- If there isno balance in the Additional Paid-in Capital from Treasury Stockaccount, the entire debit will reduce retained earnings.

- Management may decide to retire treasury stock in balance sheet.

- Notice how the accounting is the same for common and preferred stock.

This means that the stock is issued without assigning a stated value. Therefore, the amount that a corporation received, both cash or non-cash assets, becomes the legal capital; hence such amount is recorded entirely as common stock. When par value stock is issued at a discount, the assets received both cash or noncash assets is lower than the value of the common stock.

In accounting, when the company issues the common stock, its price will be used to compare with the par value or stated value of such stock before the journal entry is made. Basically, the accounting for issuance of a common stock affects the contributed capital accounts; however, nothing impacts the retained earnings. In the later section below, we will illustrate how to record the journal entry for the issuance of common stock. This includes the issuance at par value, at no par value, at a stated value, and the issuance for non-cash assets. A few months later, Chad and Rick need additional capital todevelop a website to add an online presence and decide to issue all1,000 of the company’s authorized preferred shares. The Cash accountincreases with a debit for $45 times 1,000 shares, or $45,000.

For example, on January 1, we hire an attorney to help in forming the corporation in which they charge us $8,000 for the service. However, instead of paying cash, we give the 1,000 shares of common stock to the attorney in exchange for the service instead. The measurement of the fair value of the service in the case of issuing the common stock for the services is the same as above. So, the fair value of the shares of the common stock given up will be used as the measurement if its market value is available. However, if the fair value of the shares of the common stock giving up cannot be determined, the fair value of the service expense will be used instead.

It means the stockholder has the right to control and change the company structure and policy. DeWitt carries the $ 30,000 received over and above the stated value of $200,000 permanently as paid-in capital because it is a part of the capital originally contributed by the stockholders. However, the legal capital of the DeWitt Corporation is $200,000. DeWitt carries the $ 30,000 received over and above the stated value of $200,000 permanently as paid-in capital because it is a part of the capital originally contributed by the stockholders.

On top of that, the accounting for the issuance of common stock differs from other sources. This accounting treatment also differentiates this finance source on the balance sheet. Before understanding the accounting for the allotment of common stock, it is crucial to know what it is. 5As mentioned earlier, the issuance of capital stock is not viewed as a trade by the corporation because it merely increases the number of capital shares outstanding. That is different from, for example, giving up an asset such as a truck in exchange for a computer or some other type of property. To illustrate, assume that a potential investor is willing to convey land with a fair value of $125,000 to the Maine Company in exchange for an ownership interest.

For a large corporation, this is based on a decision by its Board of Directors, a group elected to represent and serve the interest of the stockholders. Authorization is just permission to sell shares of stock; no action has actually taken place yet. Therefore, there is no journal entry for a stock authorization. This is often done by selling stocks or bonds, which represent an ownership stake in the company. The company can sell equity stock to the public by listing it on the capital market.

Par value gives the accountant a constant amount at which to record capital stock issuances in the capital stock accounts. As stated earlier, the total par value of all issued shares is generally the legal capital of the corporation. Shares with a par value of $5 have traded (sold) in the market for more than $600, and many $100 par value preferred stocks have traded for considerably less than par.

It has a few other activities, but we make these up as we go along. In each country, there are different laws and regulations that govern how shares can be traded and owned. There are different requirements for shares exchanged privately compared to when shares are traded publicly on exchanges, like the New York Stock Exchange or the London Stock Exchange.